Japan IT Services Market: Analysis By Service Type (IT Consulting & Systems Integration (SI), Application Development & Maintenance (ADM), Infrastructure & Cloud Services, Managed Services & Outsourcing (ITO/MSP), Business Process Outsourcing (BPO), Security/Cybersecurity Services, Digital / Emerging Tech Services, Others); Delivery Model (Onshore / Domestic Delivery, Nearshore, Offshore, Build-Operate-Transfer (BOT), GCC (Global Capability Center); Deployment (Cloud (Public, Private, Hybrid), On-Premises, Edge); Technology (AI/ML & Automation, Data & Analytics /BI, Cybersecurity, Cloud-Native Platforms / Devops, IoT/OT Integration, RPA / Process Automation, Others);Organization Size (Large enterprises and SMEs); Industry Verticals (Banking & Financial Services (BFSI), Telecom, Manufacturing & Automotive, Retail & e-commerce, Healthcare & Life Sciences, Public / Government, Energy/Utilities, Transport & Logistics, Media & Entertainment, Others); Region— Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 19-Dec-2025 | | Report ID: AA12251613

Market Scenario

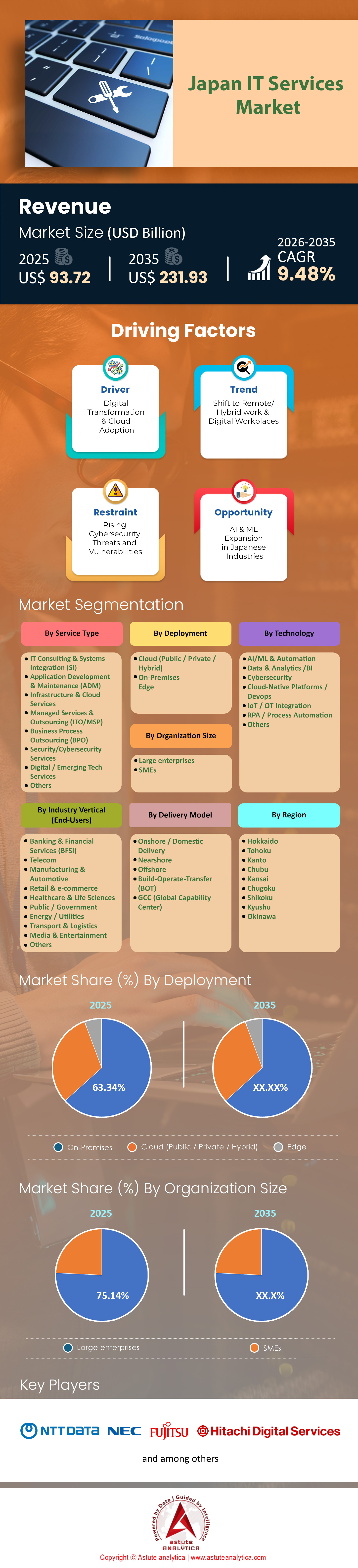

Japan IT services market size was valued at US$ 93.72 billion in 2025 and is projected to hit the market valuation of US$ 231.93 billion by 2035 at a CAGR of 9.48% during the forecast period 2026–2035.

Key Findings

- Based on service, the IT Consulting & SI holds 26.68% in 2025. However, it is projected to drop to 24.05% by 2035.

- Based on technology, AI/ML & automation emerges as the largest technology segment with a 24.92% share within the market.

- Based on delivery model, onshore/domestic delivery overwhelmingly dominates the Japanese market with a share of 70.27%.

- Based on deployment, on-premises deployments dominate the Japanese IT services market with a substantial share of 63.34%.

- Kanto region dominates the market with a substantial 47.20% share.

The structural urgency shaping the Japan IT services market in 2025 is rooted in an unavoidable deadline often referred to as the “2025 Digital Cliff.” For decades, Japanese corporations have depended on heavily customized, on-premise legacy systems that evolved into “black boxes” of unmaintainable code. According to the Ministry of Economy, Trade and Industry (METI), failure to modernize these systems could result in an annual economic loss of nearly US$ 80 billion.

The market’s momentum is no longer about pursuing innovation—it’s about survival. As specialized engineers familiar with 30-year-old COBOL systems approach retirement, organizations are racing to migrate their core functions to the cloud. This urgency has triggered a wave of investment in system integration and consulting services, as enterprises aim to leapfrog directly into the era of artificial intelligence and next-generation automation.

To Get more Insights, Request A Free Sample

Which Specific Service Categories are Leading the Charge in the Current Transformation

Managed Services and Cybersecurity currently stand out as the most rapidly expanding segments in Japan’s IT services market landscape. The shift to managed services marks a fundamental cultural change: corporations are moving away from hardware ownership toward subscription-based support models that offset internal skill shortages.

According to the 2025 IDC Japan IT Services Forecast, demand for managed cloud services is rising at double-digit rates as firms outsource the growing complexity of multi-cloud environments. Meanwhile, cybersecurity spending has intensified after the National Police Agency investigated 114 major ransomware incidents recently. For industries such as manufacturing and finance, around-the-clock Security Operations Centers (SOCs) have become an operational necessity.

Where are the Primary Geographic and Industrial Hubs of This Digital Revolution Located

The demand for high-end IT integration in the Japan IT services market is concentrated along the Taiheiyo Belt, which spans Tokyo, Nagoya, and Osaka. Tokyo remains the epicenter, propelled by the Digital Agency’s ambitious “Government Cloud” initiative that seeks to migrate 1,788 local government systems into a unified digital framework.

Elsewhere, Nagoya is witnessing a boom driven by the automotive sector’s integration of 5G-enabled IoT sensors to counteract factory labor shortages. In Osaka, pharmaceutical and chemical enterprises are leading adoption of blockchain-based supply chain systems. Across these regions, rapid expansion of Edge Data Centers has raised total IT load capacity to 1.4 gigawatts in 2025, enabling faster, localized data processing near production hubs.

Who are the Four Institutional Titans Steering The Future Of Japanese Technology

Four domestic giants dominate the competitive landscape of Japan’s IT services market. NTT Data remains the clear leader, anchoring national infrastructure projects such as the My Number card system and major public-sector cloud migrations. Fujitsu has repositioned itself under the “Uvance” brand, channeling growth into sustainability-linked transformations, particularly in retail and healthcare.

NEC Corporation has solidified leadership in biometric security, supporting the facial recognition backbone for 94 million digital ID holders. Meanwhile, Hitachi, through its “Lumada” platform, is pioneering the convergence of industrial systems with advanced analytics. Collectively, these firms are transitioning from labor-based contracts to outcome-driven, platform-centric partnerships that deliver higher margins and scalability.

What Cutting-Edge Applications are Domestic Enterprises Adopting at A Breakneck Pace

Japan’s digital transformation is concentrated around three high-impact technologies: Generative AI, Digital Identity systems, and sovereign-grade SaaS solutions. Following a nationwide administrative modernization drive, the My Number Card now functions as a “super-app” of the public sector, integrating identity verification for over 200 private applications.

In corporate environments, localized Large Language Models (LLMs) that align with Japanese linguistic and privacy standards are being swiftly implemented. Research by GMO reveals that 43% of business tasks in the services industry now leverage AI-assisted document creation. Meanwhile, enterprises are migrating to advanced ERP platforms such as SAP S/4HANA, spurred by looming support deadlines for older software versions—a shift forcing widespread financial system upgrades.

What are the Most Significant Trends and Opportunities Emerging Within The Sovereign Cloud Landscape

The emergence of Sovereign Cloud frameworks is transforming Japan’s IT services market into one of the most opportunity-rich arenas globally. Heightened geopolitical awareness and stricter data residency requirements are driving organizations to seek alternatives to foreign hyperscalers.

This shift has empowered domestic firms such as Sakura Internet, the first to earn certification as a government cloud provider. A parallel market is forming for Cloud Brokerage Services, where providers manage hybrid models blending global hyperscaler capabilities with the compliance and security of sovereign infrastructure. Going forward, data autonomy will remain a top procurement priority through at least 2026.

How are Sustainability Trends and Opportunities Creating A New Frontier For Green Data Centers

Sustainability has moved from a secondary objective to a dominant theme in the Japan IT services market. Under the nation’s 2050 carbon neutrality pledge, data center operators face mounting pressure to minimize power usage and environmental impact, propelling demand for Green IT consulting.

Recent studies indicate that 65 data centers in the Tokyo region successfully transitioned to 100% renewable energy by late 2024. Providers implementing liquid-cooling systems—such as NEC, which recently deployed 12,000 liquid-cooled racks—are securing large-scale ESG-focused contracts. Emerging “Green Hub” zones in northern regions like Hokkaido are drawing investor interest thanks to their natural cooling advantages and reduced energy costs.

What Does The Future Hold For Mid-Sized Enterprises Within the Digital Ecosystem

While major corporations dominate infrastructure investments in the Japan IT services market, Small and Medium Enterprises (SMEs) are rapidly accelerating digital adoption. Around 1,200 managed service providers now specialize in No-Code and Low-Code solutions tailored to the SME segment.

This technology democratization enables smaller firms to automate labor-intensive administrative workflows and keep pace with national digital mandates. As the government pushes forward with paperless taxation and procurement, every enterprise—regardless of size—is becoming digitally integrated. This broad participation ensures sustained, predictable demand for IT services across all tiers of Japan’s economy.

Segmental Analysis

Strategic Consultation and System Integration Pillars Supporting Robust Japanese Enterprise Modernization Efforts

Based on service, the IT Consulting & SI holds 26.68% share of the Japan IT services market. However, it is projected to drop to 24.05% by 2035. But still will keep dominating the Japanese market. Japan’s enterprise modernization journey is underpinned by extensive strategic consultation and complex system integration initiatives. Currently, more than 450 major financial institutions are engaged in core legacy system migration programs designed to enhance digital fluidity. System integrators lead over 1,200 active ERP modernization contracts across the manufacturing sector, streamlining operational workflows and performance efficiency. Large corporations typically allocate around US$ 15 million for bespoke software integration within automotive supply chains—ensuring they maintain global competitiveness in a rapidly shifting environment.

Professional consulting firms employ approximately 85,000 certified SAP practitioners, reflecting the high level of precision required in domestic migration projects in the Japan IT services market. Major system integration (SI) initiatives, particularly those within the public sector, span an average duration of 18 months. Although SI services account for 26.68% of market share in 2025—projected to decline modestly to 24.05% by 2035—their strategic significance remains deeply rooted in Japan’s modernization framework.

Long-term modernization efforts also emphasize national-level digital identity integration, where 35 leading vendors ensure civic reliability and infrastructure security. Global consulting giants operate 22 specialized innovation labs in Tokyo, dedicated exclusively to SI research and technological co-development. In the retail space, organizations typically maintain around nine legacy systems requiring continuous SI maintenance to avoid transactional disruptions. High-tier integrators handle approximately 4,500 monthly service tickets for utility firms, ensuring operational stability across Japan’s energy grid. Meanwhile, average SI contract values within logistics firms hover around US$ 8 million per engagement. Specialized consultants and technical experts play a central role in mitigating operational risks—bridging complex interdependencies between outdated mainframes and new-generation applications across the Japan IT services market.

Artificial Intelligence and Intelligent Automation Driving High Performance Industrial Manufacturing Portfolios Successfully

Based on technology, AI/ML & automation emerges as the largest technology segment with a 24.92% share in the Japan IT services market. Artificial intelligence and intelligent automation have become core enablers of Japan’s industrial renaissance. Manufacturing facilities now employ more than 12,000 collaborative robots equipped with AI-powered vision systems to enhance quality control and productivity. Financial institutions leverage around 550 AI models for real-time fraud detection, significantly reducing cybercrime exposure. Retail networks deploy 2,800 automated shelf-stocking sensors utilizing machine learning for precise inventory management, while Japanese tech firms continue to advance domestic innovation with roughly 950 AI-related natural language processing patent filings each year.

Customer engagement has also evolved, with 6,400 AI-driven chatbots now providing 24/7 support across e-commerce platforms. Collectively, such advancements anchor a 24.92% market share for specialized technology segments within Japan’s broader IT ecosystem. Smart logistics operations employ about 1,500 autonomous guided vehicles to optimize supply chain flows, and leading enterprises allocate close to US$ 12 million annually toward internal AI research departments aimed at driving innovation and competitiveness.

The healthcare sector demonstrates another clear application, with 320 AI diagnostic systems supporting oncological decision-making and improving treatment outcomes. Major shipping ports leverage 80 automated crane systems to achieve faster container processing and operational consistency. At the same time, over 2,100 concurrent automation pilots are active across Tokyo’s metropolitan area, focusing on urban optimization. Growth in the Japan IT services market increasingly depends on automation-driven gains in both industrial and office environments, with real-time data processing now a key driver of energy efficiency across large commercial infrastructures.

Localized Delivery Models Ensuring Cultural Synergy and Data Security for Domestic Enterprises

Based on delivery model, onshore/domestic delivery overwhelmingly dominates the Japanese IT services market with a share of 70.27%. Japan’s localized IT delivery framework remains a cornerstone of cultural synergy and client trust. Tokyo alone hosts around 4,800 domestic IT service providers that cater to immediate local demand. Language precision plays an essential role—each project team includes roughly 100 native Japanese-speaking professionals to ensure effective communication and flawless execution. Close to 350 regional data centers minimize latency while supporting localized enterprise applications, and traditional business culture often calls for up to 15 face-to-face meetings before finalizing contracts to build long-term rapport.

Onshore delivery dominates the Japan IT services market with a commanding 70.27% market share, supported by an extensive workforce of 250,000 support staff providing real-time hardware troubleshooting and assistance. Security remains non-negotiable—government contracts require 12 distinct clearance levels for personnel managing sensitive public-sector data. Furthermore, service providers operate 90 satellite offices to serve secondary urban markets beyond Tokyo.

On any given day, local teams handle around 14,000 infrastructure maintenance operations vital to sustaining Japan’s national economy. Domestic firms collectively hold over 75,000 certifications aligned with regional regulations and industry standards. Annual spending of roughly US$ 20 million on local training programs reinforces business etiquette and ensures cultural alignment between vendors and clients. The Japan IT services market continues to thrive on proximity, trust, and shared cultural values—factors that remain critical in securing and retaining high-value enterprise contracts.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Infrastructure Resilience and Private Server Infrastructure Anchoring Modern Enterprise Technology Frameworks Daily

Based on deployment, on-premises deployments dominate the Japanese IT services market with a substantial share of 63.34%. Infrastructure resilience and private data environments remain foundational to Japan’s enterprise technology framework. Data sovereignty considerations lead major financial institutions to maintain approximately 450 private server farms dedicated to secure information storage. In parallel, manufacturing units operate 1,200 edge servers to support real-time production control and efficient data management. Collectively, enterprises deploy around 85,000 physical server racks within corporate facilities to ensure complete oversight and system reliability.

Stringent security measures form the backbone of this architecture, with up to 12 layers of physical access control at on-premises data centers. Japan’s major banks run over 3,200 critical applications on internal mainframes to maintain stability within legacy banking systems—accounting for a substantial 63.34% of hardware deployment share.

Operational maintenance remains equally intensive. Large corporations routinely allocate about US$ 5 million annually to cooling, power, and related infrastructure. Internal IT teams handle over 15,000 physical backup tapes for disaster recovery, ensuring business continuity in the Japan IT services market. Sensitive government tasks operate across 220 isolated LAN environments, while research institutions maintain 18 private supercomputers for advanced computation independent of public cloud dependence.

Hardware refresh cycles span roughly 36 months, requiring meticulous planning to coordinate upgrades and hardware replacements. Reliability and sovereignty define this domestic IT environment, especially among industrial and government organizations prioritizing control and security over external cloud solutions. Dedicated private infrastructure continues to safeguard national data integrity—acting as an enduring anchor within the Japan market.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Economic Powerhouse Kanto Region Consolidates Market with over 47.20% Revenue Contribution

Tokyo continues to function as the unchallenged gravitational core of the Japan IT services market. Nearly 90% of all publicly listed corporations across the nation are headquartered within the Kanto region, giving the local economy unrivaled strategic weight. This high corporate concentration creates a powerful self-reinforcing ecosystem, supported by the steady influx of more than 120,000 fresh IT graduates each year. Their entry sustains a steadily expanding professional workforce and keeps pace with rising enterprise technology demands.

Infrastructure maturity across the Japan IT services market stands out as a defining advantage. Roughly 75% of Japan’s total data center capacity is clustered within the Greater Tokyo Area, ensuring ultra-low latency for financial institutions and corporate data hubs. The Tokyo-based Digital Agency channels roughly US$ 20 billion in yearly public procurement spending, a flow of capital that directly benefits the region’s system integrators and cloud infrastructure providers.

Strong international interest further accelerates this dominance—Kanto attracts around 80% of all foreign direct investment entering Japan’s technology sector. Ambitious government-led initiatives, particularly under the Digital Garden City program, have already catalyzed more than 1,500 ongoing infrastructure and modernization projects in the region. With a commanding 47.20% market share secured through 2025, Kanto’s role as Japan’s digital and economic powerhouse remains firmly entrenched.

Industrial Innovation and Resilient Infrastructure Propel Kansai Region Growth in Japan IT Services Market

The Kansai region, anchored by Osaka and Kyoto, has emerged as Japan’s strongest secondary technology hub, commanding a 17.44% share of the national IT services market. Its rise is grounded in both innovation and resilience. Osaka, in particular, leads disaster recovery infrastructure with 45 active redundancy sites dedicated to financial institutions seeking risk diversification beyond the Kanto corridor.

The 2025 Osaka World Expo acted as a major inflection point, igniting roughly 500 smart city pilot projects that integrate IoT ecosystems into municipal infrastructure. Kyoto’s longstanding manufacturing excellence sustains this growth trajectory — with about 1,200 precision engineering companies specializing in automation components and industrial IoT. This concentration of advanced manufacturing expertise has evolved into a niche segment within the Japan IT services market, focused on digital factory transformation and high-performance industrial software.

Massive regional investments continue to elevate Kansai’s technological competitiveness. The US$ 5 billion Umekita 2nd Project serves as a flagship mixed-use innovation district, encouraging collaboration between established corporates and emerging development startups. Eight major academic institutions have also partnered with regional IT firms, converting academic research breakthroughs into commercial applications. Collectively, these efforts ensure Kansai contributes 20% of Japan’s total electronics output—fortifying its role as a resilient, innovation-driven engine within the national technology landscape.

Recent Developments Shaping the Japan IT Services Market

- Fujitsu's Mission Critical Transformation (Oct 10, 2025): Fujitsu migrated its service operations virtualization platform—serving 3,000 enterprise clients—to Nutanix Cloud Infrastructure. This achieved 30% cost savings and 90% labor reduction, enabling scalable hybrid environments. The company launched a new "Mission Critical Transformation Service" to help others replicate these gains.

- Fujitsu, SEKISUI CHEMICAL, SAP Japan Collaboration (Oct 17, 2025): SEKISUI CHEMICAL partnered with Fujitsu and SAP Japan to deploy SAP S/4HANA Cloud across 100+ global subsidiaries starting April 2025. The initiative modernizes management systems for real-time data insights, enhancing decision-making in chemical manufacturing.

- Fujitsu Cloud Service Generative AI Platform (Feb 13, 2025): Fujitsu introduced a secure GenAI platform for enterprises, allowing private data processing without external exposure. Trials commenced in Japan during FY2025, targeting compliance-heavy sectors like finance and healthcare.

- NTT DOCOMO BUSINESS Gartner Award (Oct 22, 2025): NTT DOCOMO BUSINESS became Japan's first recipient of the APAC Gartner "Eye on Innovation Award" for its business solutions platform. The recognition highlights innovative IT services driving digital transformation for corporate clients.

- NEC Cybersecurity Center Expansion (Dec 15, 2025): NEC announced enhancements to its cybersecurity operations center, launched in May 2025, to safeguard Japan's digital infrastructure against rising threats. The facility bolsters national cyber resilience with advanced threat intelligence.

Top Players in the Japan IT Services Market

- Fujitsu Limited

- Hitachi Ltd.

- NEC Corporation

- NTT DATA Corporation

- IBM Japan Ltd.

- Accenture plc

- Itochu Techno Solutions Co., Ltd.

- SCSK Corporation

- DTS Corporation

- Other Prominent Players

Market Segmentation Overview

By Service Type

- IT Consulting & Systems Integration (SI)

- Application Development & Maintenance (ADM)

- Infrastructure & Cloud Services

- Managed Services & Outsourcing (ITO/MSP)

- Business Process Outsourcing (BPO)

- Security/Cybersecurity Services

- Digital / Emerging Tech Services

- Others

By Delivery Model

- Onshore / Domestic Delivery

- Nearshore

- Offshore

- Build-Operate-Transfer (BOT)

- GCC (Global Capability Center)

By Deployment

- Cloud (Public / Private / Hybrid)

- On-Premises

- Edge

By Technology

- AI/ML & Automation

- Data & Analytics /BI

- Cybersecurity

- Cloud-Native Platforms / Devops

- IoT / OT Integration

- RPA / Process Automation

- Others

By Organization Size

- Large enterprises

- SMEs

By Industry Vertical (End Users)

- Banking & Financial Services (BFSI)

- Telecom

- Manufacturing & Automotive

- Retail & e-commerce

- Healthcare & Life Sciences

- Public / Government

- Energy / Utilities

- Transport & Logistics

- Media & Entertainment

- Others

By Region

- Hokkaido

- Tohoku

- Kanto

- Chubu

- Kansai

- Chugoku

- Shikoku

- Kyushu

- Okinawa

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |